Online payment habits are part of everyday digital life now. People send invoices, receive email receipts, manage app subscriptions, and move money from one phone. That convenience also creates small risks. A missed receipt can cause confusion later. A saved card can stay active on a shared device. A weak notification setup can hide account messages. Payment-related apps need more care than casual tools because money and identity sit close together. Good habits help users keep deposits, alerts, receipts, and account settings easier to track.

Deposit options should be checked before use

Anyone reading about parimatch deposit methods should treat payment setup as an account safety task. Deposit options can vary by region, account status, and platform rules. Users should read the available method details before adding money. They should check processing times, limits, fees, verification steps, and withdrawal rules. A deposit should never be made before the user understands how funds move in both directions. Clear records also matter because payment issues are easier to solve with dates and receipts.

This topic also fits readers who work with email, scripts, and digital workflows. Many payment problems start when records scatter across apps, inboxes, screenshots, and bank notifications. A user may receive an email receipt, a card alert, and an account message for one action. If those records are not organized, support questions become harder. Even a simple email folder can help. Developers may go further and use scripts to label receipts, flag payment confirmations, or store basic transaction references.

Email receipts need better handling

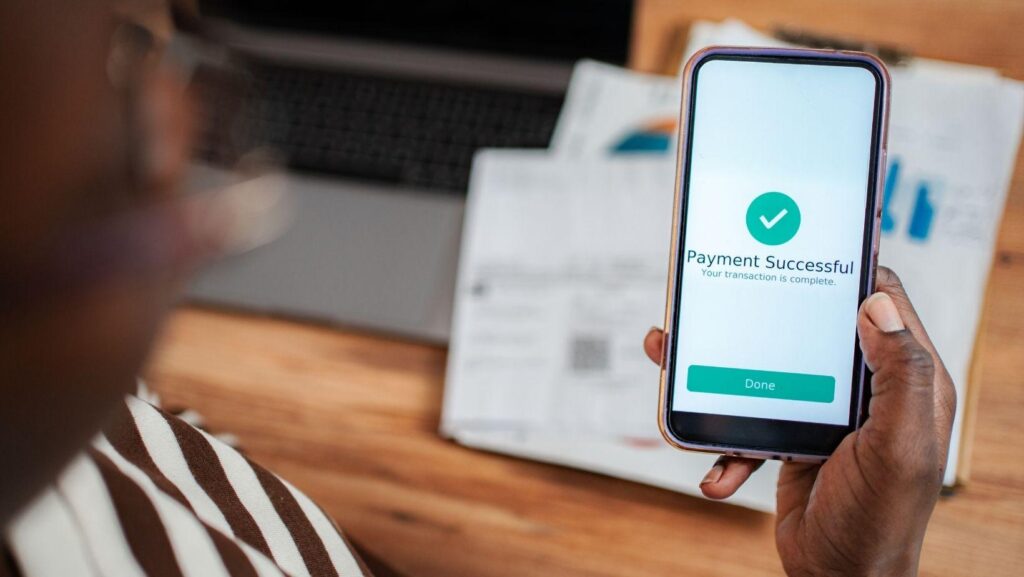

Email remains the main record for many online payments. A deposit confirmation may arrive with a timestamp, transaction number, amount, and account notice. That message can be useful later if a balance update is delayed. It can also help users compare bank activity with account history. The problem starts when receipts disappear inside crowded inboxes. Promotions, newsletters, and social updates can bury payment messages fast.

A clean inbox setup helps more than people expect. Users can create a folder for payment receipts and account alerts. They can also avoid deleting confirmations until the transaction is fully settled. Developers and technical users may automate sorting with filters or Python scripts. The goal is simple. Keep payment records easy to find. A receipt should not require twenty minutes of searching when support asks for basic proof.

What users should check before depositing

Deposits should start with a few practical checks. These checks reduce confusion and protect the account from avoidable mistakes. They also help users notice when a payment method does not match their needs. A fast option is not always the right option. Some methods may process quickly but require stricter verification later. Others may be slower but easier to document.

Before adding funds, users should check:

- The minimum and maximum deposit amount.

- Processing time for the selected method.

- Any listed fee or conversion detail.

- Verification steps before withdrawals.

- Whether the payment account belongs to the user.

- Where receipts and alerts will arrive.

Small records prevent larger disputes

Payment records matter most when something feels wrong. A balance may update slowly. A receipt may arrive before the app reflects the deposit. A bank may show a pending charge for longer than expected. Without records, the user has only memory. With records, the user can provide time, amount, method, and reference details. That makes support conversations clearer. It also helps users avoid repeating the same action while a payment is still processing.

Saved cards and shared devices need caution

Saved payment methods can make deposits faster. They can also reduce the pause before money moves. That matters on any phone used by more than one person. A family member may open an app by mistake. A child may tap a notification without knowing what it means. A lock-screen alert may show account activity to someone nearby. Users should avoid saved cards on shared phones. They should also hide sensitive notification previews.

Private devices need care too. A screen lock should be active. Two-step login should be used when available. Public Wi-Fi should be avoided during deposits or account changes. Users should also check whether browser autofill stores payment data. A private app can still leak information through general phone settings. Better payment safety comes from the whole device, not one app setting.

Automation can support cleaner finance habits

Technical users can use simple automation to stay organized. An email filter can send deposit receipts into one folder. A spreadsheet can track date, method, amount, and status. A Python script can extract receipt subjects or flag missing confirmations. These tools should never store passwords or sensitive card data. They should only help track non-sensitive references and reminders.

This kind of organization is useful beyond entertainment apps. It works for subscriptions, hosting tools, software licenses, shopping orders, and invoices. The habit stays the same. Keep payment records clean. Separate security alerts from promotional emails. Review account activity before it becomes confusing. Users who manage receipts well usually solve payment questions faster. They also notice unusual activity sooner.

Safer deposits start with slower decisions

Money-related apps should be used only by adults where local rules allow it. Users should set a fixed entertainment budget before making deposits. Money for rent, food, bills, transport, savings, or family needs should stay separate. Fast payment options can make small decisions feel too easy. A written limit or account limit creates a useful pause.

Payment habits should stay calm and deliberate. Users should avoid deposits when tired, angry, distracted, or trying to recover losses. They should keep receipts, check account history, and review payment settings often. A safer deposit process is not complicated. It starts with clear records, private devices, careful alerts, and spending limits. That approach keeps online payments easier to manage and harder to misuse.